Over 400,000 ‘buy to let’ owners now use limited companies!

Over 400,000 ‘buy to let’ owners now use limited companies!

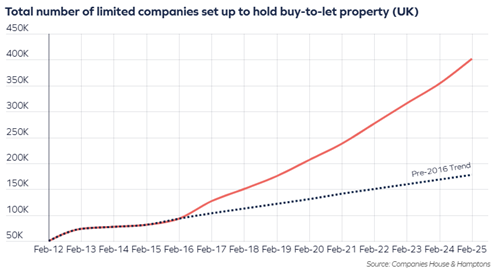

The number of limited companies set up to hold ‘buy to let’ property topped the 400,000 mark in February 2025, up by over 330% over the past nine years from only 92,000 incorporated landlords in 2016, according to analysis from a source at Companies House.

Companies House now has more registered buy to let companies than any other type of business, with four times as many company landlords as takeaways and hairdressers.

The change which came into place when the tax rules, which were first introduced in 2016 by then chancellor George Osborne, saw the virtual phasing out of full mortgage interest rate relief for landlords.

A spokesperson for a London Estate agency noted: ‘The limited company is now the structure of choice for the next generation of investors. We estimate that 70-75% of new buy to let purchases now go into a company structure, a figure that has been steadily growing, current tax rules mean that most, although not all, new investors find themselves better off in a company structure than owning an investment property in their own name’.

The key difference between owning a property personally and owning it via a company structure is that you can still deduct mortgage interest as a business expense before calculating the tax liability. This contrasts sharply with the situation for individual landlords, who since 2020 have been restricted to a 20% tax credit on mortgage interest payments.

This tax pain particularly hits higher rate taxpayers, who fall into the 40% tax bracket.

Pros and cons of corporate structure

But there are pros and cons for landlords considering whether to use a company rather than direct ownership.

In terms of tax rates, a company is, on the surface, a better proposition!

This is because the main rate of corporation tax is set at 25% for companies with profits of at least £250,000, applying to both income profits and capital gains. Where profits are less than this figure, the rate varies from 19–25%.

By contrast, individual landlords are subject to rates of 20% (basic), 40% (higher) and 45% (additional) on their rental profits as well as potentially capital gains.

However, while the corporate rates appear more attractive, one needs to bear in mind that there is an additional layer of tax payable by shareholders when the company pays out rental profits by way of dividend.

Dividends are then taxed at rates of 8.75%/33.75%/39.35% depending on your taxable income.

Making Tax Digital for landlords

From April 2026, landlords will also face more red tape with changes to the tax rules with the introduction of Making Tax Digital (MTD) for Income Tax, which will require taxpayers with rental income over £50,000 a year forced to file quarterly returns with HMRC. This will be rolled out to those earning £30,000 in April 2027.

HMRC will be sending letters to landlords whose 2023-24 self-assessment tax return showed their rental income was close to, or over, £50,000 telling them they may need to use MTD from April 2026. This means the first MTD quarterly report would have to be filed with HMRC by 1 July 2026.

If you need any help or advice when you are buying a property to rent out, please get in touch with us at Kennedys Accounting – please see our other blogs and information on this subject on our website including https://kennedysaccounting.uk/landlords-look-out-for-making-tax-digital-letters-insights/