Pros and cons of PAYE salary, dividends or a combination of both – what is best for company directors?

Pros and cons of PAYE salary, dividends or a combination of both – what is best for company directors?

With several tax changes coming into play, have you considered and discussed with your accountant the plan for this tax year (2025/26).

So, to start with, let’s look at some of those important changes which may impact how directors pay themselves.

Shareholders in owner-managed businesses also need to be aware of new ‘dividend disclosure rules’ which will come into force for the 2025-26 tax year. This means that if you are a director holding shares in a company, you will need to report dividend income received from your own companies, and the percentage shareholding held in those companies on your self-assessment.

From April 2025, self-employed individuals must declare when any self-employment commenced or ceased. although the exact reporting mechanism is not yet clear.

National insurance and employment allowance

One of the significant changes involves employers’ National Insurance (NI) contributions. Key things to note are that the threshold has reduced from £9,100 to £5,000, and the rate has increased to 15% (as reported in our previous insights). However, on the positive side, the employment allowance has increased from £5,000 to £10,500, and the eligibility threshold that restricted it to smaller employers has been removed.

However, please note, to claim this allowance, you must have at least two directors/employees on a salary over £5,000. Single directors with no other employees on payroll cannot claim it. Furthermore, if you have multiple connected companies and payrolls, the allowance can only be claimed once against one payroll – an important consideration for those with group companies.

Salary vs dividends: comparing the numbers

The positives of salaries and dividends are well-known, but it is not a ‘one size fits all’ approach and needs to be considered as to which is best for individuals depending on their circumstances.

Salaries offer uniformity as well as potentially pension benefits and can also reduce corporation tax, while dividends provide tax advantages with lower rates and no National Insurance contributions.

It’s also worth noting that the dividend allowance remains at £500 for 2025/26, but of course dividends can only be paid if profits are available.

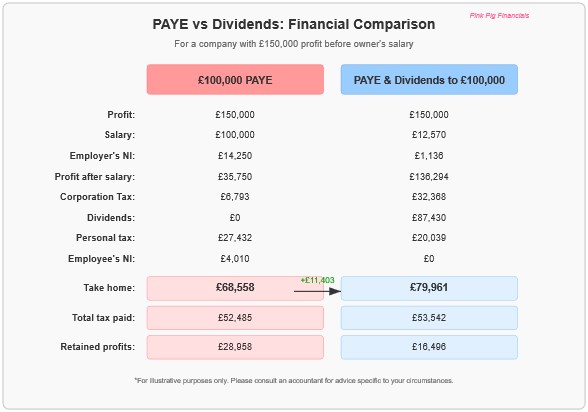

Below is an example for a limited company with £150,000 profit before any owner’s salary. This assumes no other employees are on payroll (meaning the employment allowance cannot be claimed) and ignores payments on account for personal tax. It also assumes the owner has no other income and is on a standard tax code.

If you take a look at the numbers, the dividend route provides a higher take-home pay (£79,961 vs £68,558), although the total tax paid is marginally higher with dividends (£53,542 vs £52,485).

The salary approach leaves considerably more retained profit in the business (£28,958 vs £16,496), which could be valuable for future investment.

What is the right decision

Ultimately, the right decision depends on your personal and business goals. Both options would qualify for state pensions under NI, and both would allow you to get a mortgage (subject to the usual affordability tests etc). Salaries are also helpful for budgeting and planning purposes as it allows you to keep a consistent cashflow.

Dividends may allow you to maximise your take-home pay as well as having sufficient profits to support dividend payments, you may also prefer to minimise NI.

Many directors find that a balanced combination offers the best of both worlds, providing some regular income while maximising overall returns and maintaining flexibility in how profits are extracted, but it really is down to the individuals’ circumstances and their business plans and it’s important that this is discussed with your accountant who can give you advice that is right for you.

As with most financial business decisions, there is no one-size-fits-all answer! The best approach depends on your circumstances, goals and the financial health of your business.