Domestic Reverse Charge VAT

Domestic Reverse Charge VAT

VAT reverse charge rules came into effect on 1st March 2021, which altered the way businesses operating the Construction Industry Scheme (CIS) and are VAT registered complete their invoices.

These rules can feel complex, and you need to be aware of what they may mean for your business sales invoices and VAT returns.

Let’s start with ‘What is the VAT reverse charge?’

The reverse charge is a way of accounting for VAT where the ‘end-customer’ accounts for VAT and the supplier of construction services doesn’t. The reverse charge means the end-customer receiving construction services has to pay the VAT to HMRC instead of the supplier. The end-customer recovers VAT subject to the normal rules set by HMRC.

How does domestic reverse VAT work?

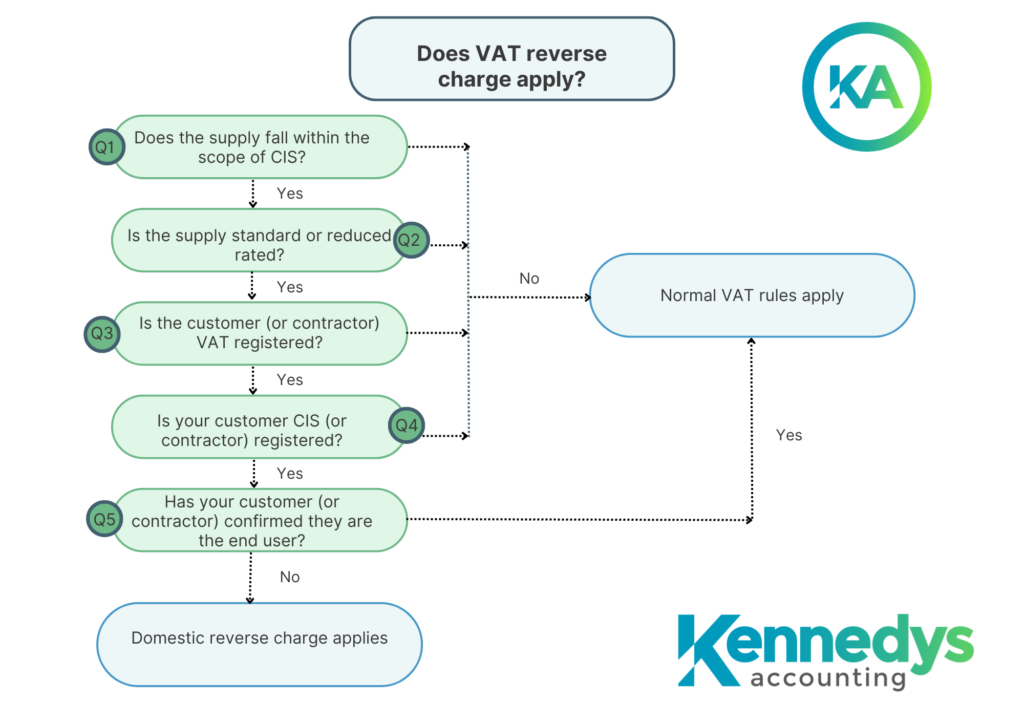

The new rules apply to standard rate VAT or reduced-rate construction services provided by VAT registered businesses. The reverse charge doesn’t apply to supplies of services which are zero-rated, such as the construction of housing. If you don’t make an onward supply of construction services, you won’t have an end-customer and normal VAT rules apply.

If your invoices have both CIS and non-CIS registered supplies, the reverse charge applies to the whole invoice amount.

An example where the reverse charge applies is where a sub-contractor supplies services to a customer (or contractor) who then makes an onward supply of the same construction services to an end-customer. All parties in the chain are VAT registered. When the end-customer confirms they are the end of the supply chain, normal VAT rules apply.

You can use the following flowchart to work out if you should apply the reverse charge or whether normal VAT rules apply.

What do I have to do?

If you are a subcontractor

If you’re invoicing a customer (or contractor) in a supply chain, you’ll either have to charge VAT as normal or apply the reverse charge. For the reverse charge, your invoice total will not include VAT.

However, your invoice must include a statement advising your customer (or contractor) that the reverse charge rules apply, stating the amount of output VAT to be applied (20% if it’s the standard rate of VAT). Your customer (or contractor) will need to include that amount on their VAT return. You don’t include anything on your VAT return about the reverse charge.

If you are a main contractor

If you’re a main contractor receiving a VAT reverse charge invoice from a subcontractor, you should continue to record it as a normal expense invoice and include input VAT on your VAT return.

You’ll also need to account for the reverse charge VAT the subcontractor has notified you about. The overall effect on your VAT liability is neutral as the output VAT is covered by the input VAT.

What else do you need to consider?

It may be possible to be a subcontractor on one project and a main contractor on another, so you need to consider the VAT status of your services for each construction project you work on.